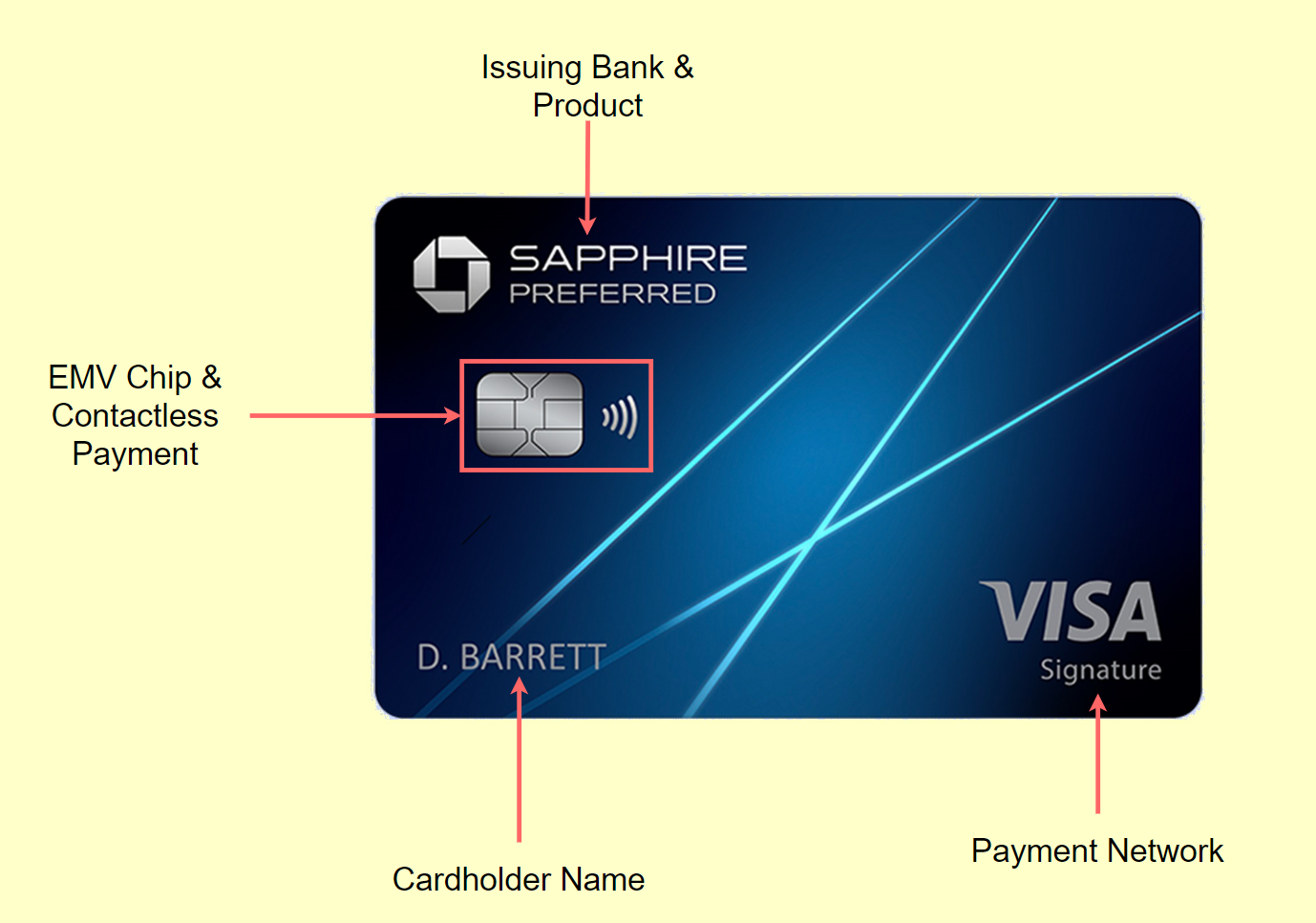

#4 Anatomy of a Modern Credit Card

(January 2024)

-

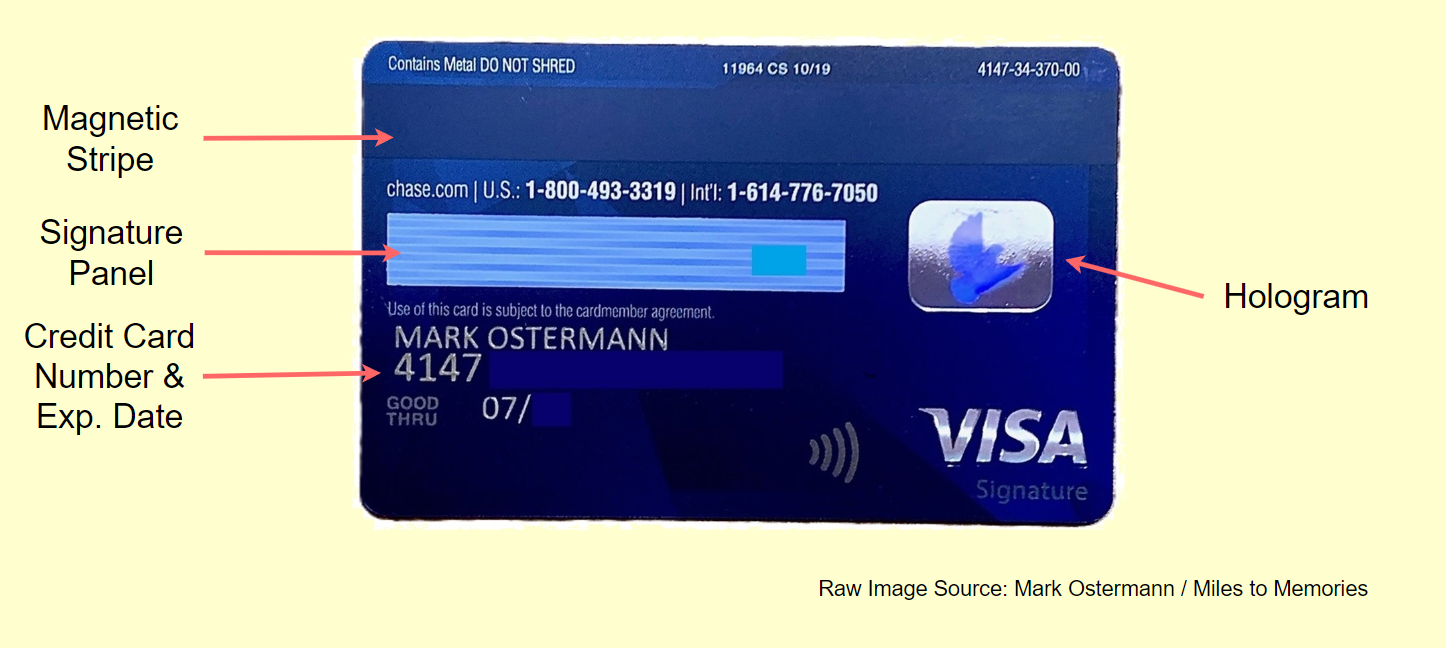

The credit card number might have moved from the front to the back of the card.

-

The signature hologram stickers have also largely moved to the back of the card.

-

Now present on almost all credit cards are EMV chips, enabling contactless and more secure payments.

-

Magnetic Strip: The magnetic strip contains a static (unchanging) set of Card Holder Details (CHD) and Sensitive Authentication Data (SAD). A transaction will fail if both sets of data can’t be read off the strip. Since this data is unchanging, it’s fairly easy to have it stolen by a bad actor, especially during a physical transaction where they can reuse the same data set to perform unauthorized transactions on your card.

-

EMV Chip: A small microprocessor embedded in the chip generates a unique, one-time code for each transaction when inserted into a chip card reader or tapped for a contactless payment. This is unlike the static data contained on a magnetic stripe. When you use your card at a terminal, the chip interacts with the merchant's point-of-sale system to create a transaction code that uniquely identifies that specific purchase. This code cannot be used again, making it extremely difficult for fraudsters to replicate or reuse your card details. Additionally, during the transaction, the chip and the issuing bank communicate to authenticate the transaction, ensuring that the card is valid and the person using it is authorized to do so. This dynamic process provides a robust layer of security that greatly reduces the risk of counterfeit and fraudulent transactions.

Chase Credit Card Technology

Bonus: Anatomy of a Card Number

-

Major Industry Identifier (digit 1): This digit indicates the card network and industry. For example, Visa cards often start with a 4, and Mastercard with 5 and American Express with 3.

-

Bank Identification Number (digits 2-4): The rest of the IIN identifies the issuing bank or institution. This helps in routing the transaction to the correct bank.

-

Account Number (digits 5-16): These digits represent the individual account number. Each bank has its own system for assigning these numbers, but they must be unique to each cardholder with the issuer.

-

Check Digit (digit 16): This is used as a safety check to ensure the card number is valid. It's calculated through the Luhn algorithm, a simple checksum* formula used to validate a variety of identification numbers. [*checksum: a value that represents the number of bits in a transmission message and is used by IT professionals to detect high-level errors within data transmissions]

About Dan Alvarez

Dan Alvarez began at JPMorgan Chase in June 2016 as a summer technology analyst/ infrastructure engineer, and left in April 2022 as a Senior Software Engineer in Global Technology Infrastructure - Product Strategy and Site Reliability Engineering (SRE). Since May 2022, he has worked for Amazon Web Services as an Enterprise Solutions Architect.

He is also an avid guest lecturer for the City University of New York and has given lectures on artificial intelligence, cloud computing and career progression. Dan also works closely with Amazon's Skills to Jobs team and the NY Tech Alliance with the goal of creating the most diverse, equitable and accessible tech ecosystem in the world.

A graduate of Brooklyn College, he is listed as an Alumni Champion of the school and was named one of Brooklyn College's 30 Under 30. He lives in Bensonhurst, Brooklyn.